What to expect from the latest GDP figures?

Since the ONS is publishing fresh GDP figures, it seemed timely to update my analysis looking at Google mobility data as a predictor of GDP. Now, the new ONS data will only update us up to the end of December 2021, and we are of course already well into February. So I’ll say a few things about January 2022, too. (At the time of writing, we only have 4 days of mobility data for February 2022.)

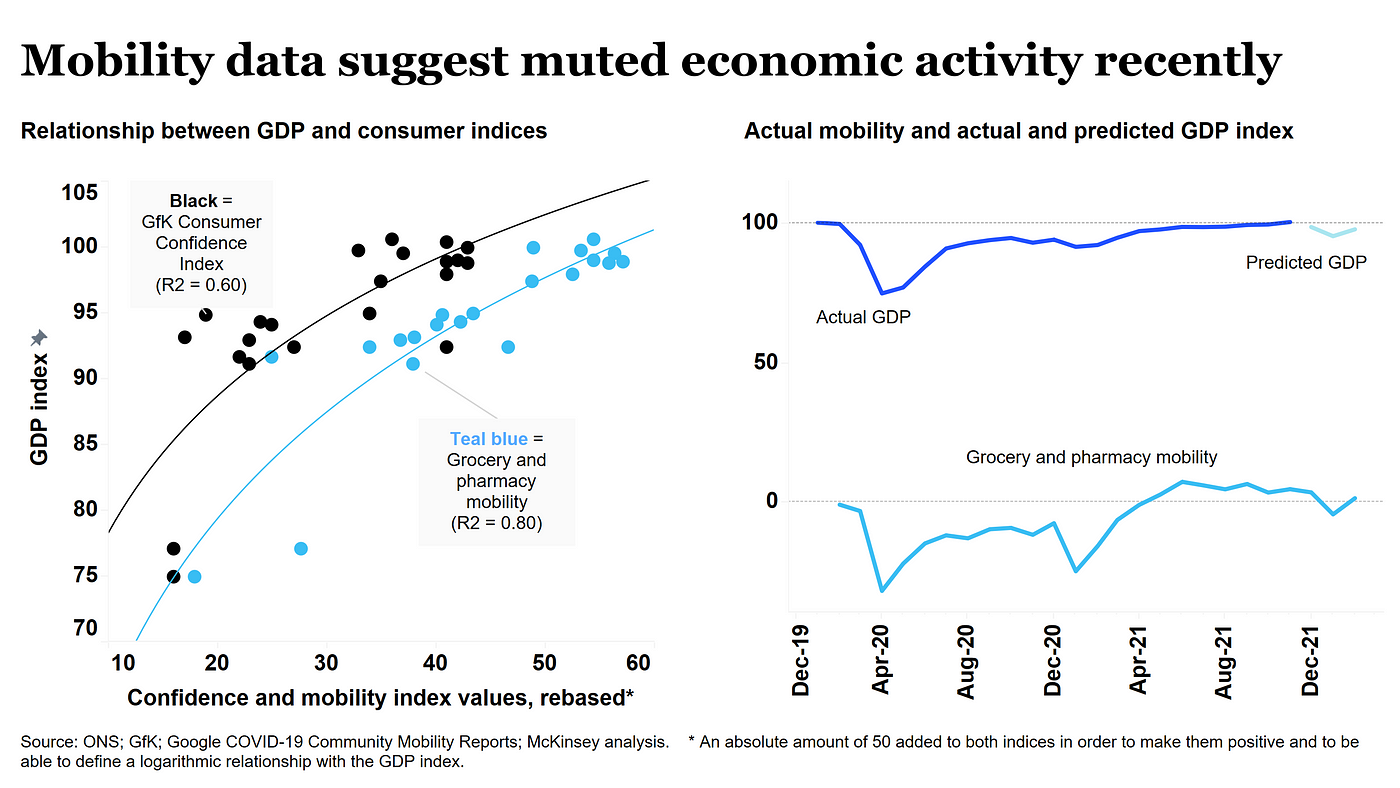

As the left hand panel of the chart shows, the Google index that tracks grocery and pharmacy mobility — essentially footfall at these types of retail stores (shown in teal blue) — has been a decent predictor of real GDP throughout the pandemic. It has performed slightly better as a predictor than, for example, the GfK Consumer Confidence Index (shown in black).

Because the mobility data is available with an average 4-day lag, it gives us some indication of what might have been going on in economic activity well befor the ONS publish their official figures. In the right hand graph, I’ve taken the December, January and February mobility data and used it to “predict” the GDP index (relative to December 2019), as shown in the light blue line.

On this simplistic basis, the economic recovery doesn’t look too promising. If we take the mobility numbers and their relationship with GDP literally, we would expect GDP to actually have dipped below its pre-pandemic levels again in December 2021 (having briefly returned to pre-pandmic levels in November 2021). Indeed, the GfK consumer confidence index for December and January was also relatively depressed.

However, the mobility index is far from perfect as a predictor. In fact, the one month that it got spectacularly wrong in that sense was January 2021. You will recall that the UK faced another lockdown back then, so mobility will have been down significantly. Yet, GDP — while not growing — didn’t dip as much as you might have expected. This could be to do with the lockdown, or the dynamics of mobility and spending in any January, post-holidays.

My best guess is that December and January figures for 2022 will look somewhat better than the simple prediction in the chart suggests. At the same time, I remain somewhat gloomy about the UK’s overall economic outlook. On one hand, things have gone a lot better than they might have done, on many fronts (e.g., employment, investment). On the other, with new clouds on the economic horizon (such as inflation), maybe we won’t see the consumption-led growth many economic forecasters in the UK have come to expect.